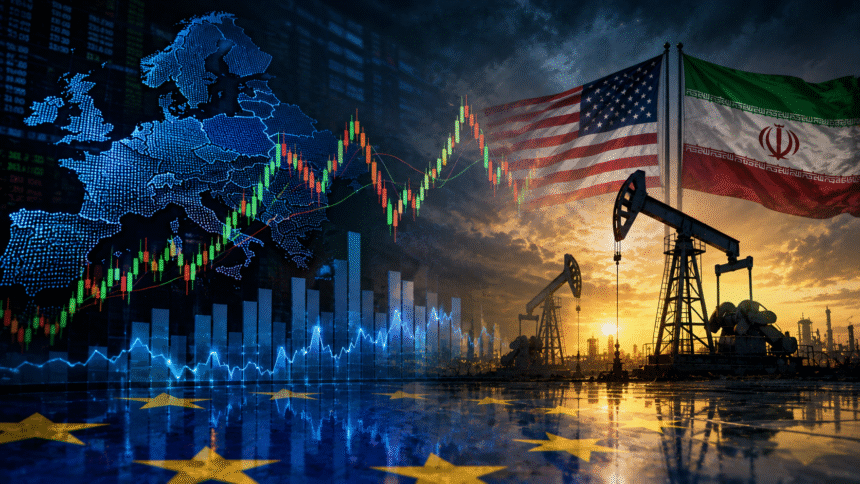

European markets moved cautiously on Monday as investors reacted to rising oil prices and uncertainty surrounding stalled U.S.-Iran talks, leaving the pan-European STOXX 600 index almost unchanged.

The STOXX 600 held near 611.68 points, reflecting a market that was neither strongly selling off nor confidently advancing. Investors appeared hesitant as geopolitical tensions increased pressure on energy prices and revived concerns about inflation across Europe.

Oil prices rose after U.S. President Donald Trump rejected Iran’s latest response to a U.S. peace proposal, a development that weakened hopes for a diplomatic breakthrough. Brent crude climbed above $105 per barrel, while U.S. West Texas Intermediate also moved higher, increasing fears that expensive energy could again become a major burden for European economies.

Europe is particularly exposed to energy shocks because many of its industries, transport networks, and households remain sensitive to fuel and gas prices. Any extended rise in oil prices could increase production costs, pressure company profits, and make it harder for central banks to control inflation.

The market reaction was cautious rather than dramatic. Some investors reduced exposure to riskier assets, while others waited for clearer signals from diplomacy, oil markets, and central banks. Reuters reported that global stocks softened and the dollar strengthened as markets assessed the stalemate in U.S.-Iran talks and renewed pressure on the Strait of Hormuz, a key route for global energy supplies.

Several European sectors came under pressure. Defence and luxury stocks were among the weaker performers, with companies such as Rheinmetall, Hensoldt, Hermès, and Burberry recording declines. Telecom stocks, however, offered some support, helped by gains in companies including BT and Vodafone.

The rise in oil prices also added pressure on the European Central Bank. If energy costs remain elevated, inflation could become more difficult to bring under control. That may complicate expectations for interest rates, especially if policymakers decide that inflation risks require a tighter monetary stance.

Despite the uncertain mood, some analysts remained optimistic about the longer-term outlook for European equities, pointing to resilient earnings and the ability of major companies to absorb short-term shocks. However, the immediate direction of markets is likely to depend on whether oil prices continue rising or diplomatic talks show signs of progress.

For now, European markets appear trapped between two forces: solid corporate performance on one side, and geopolitical risk on the other. The near-flat STOXX 600 shows that investors are not yet panicking, but they are clearly waiting for clarity before making stronger moves.