Eurozone inflation is expected to rise sharply this year before gradually returning close to the European Central Bank’s target, according to the ECB’s latest Survey of Professional Forecasters. The findings suggest that economists see the current inflation jump as serious, but not necessarily permanent.

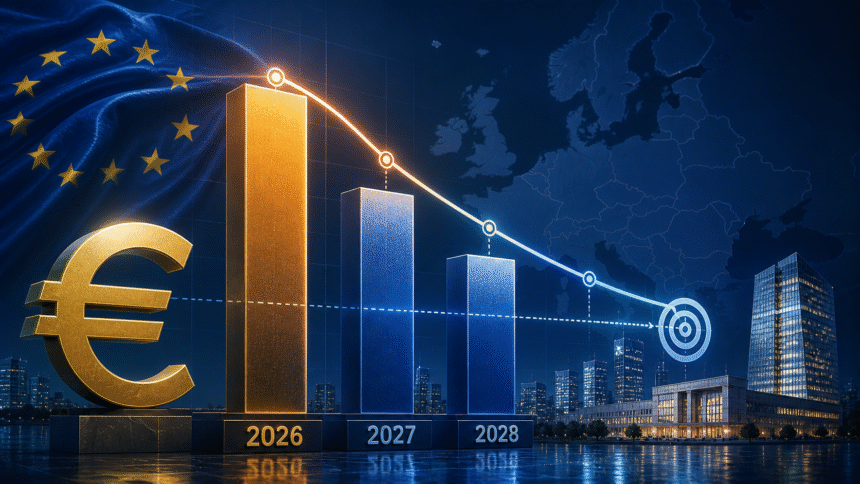

The survey expects headline inflation in the euro area to average 2.7% in 2026, a major upward revision from the previous forecast of 1.8%. However, inflation is then expected to ease to 2.1% in 2027 and return to 2.0% in 2028, in line with the ECB’s medium-term target.

The main reason behind this year’s jump is the rise in energy prices, which has been linked to the war in the Middle East. Higher oil and gas costs have increased pressure on transport, manufacturing, food production, and household bills across Europe. This has forced forecasters to revise their short-term inflation expectations upward.

Despite the higher inflation forecast for 2026, the ECB survey offers a more reassuring longer-term picture. Longer-term inflation expectations remain anchored at 2.0%, meaning professional forecasters do not yet expect the current energy shock to turn into a lasting inflation crisis.

Core inflation, which excludes volatile energy and food prices, is also expected to remain relatively controlled. The survey forecasts core inflation at 2.2% in 2026 and 2027, before easing to 2.1% in 2028. This suggests that while price pressures are spreading beyond energy, they are not yet seen as deeply embedded in the wider economy.

The inflation outlook creates a difficult challenge for the European Central Bank. On one hand, inflation is clearly above target this year, which may increase pressure on policymakers to raise interest rates. On the other hand, if inflation is expected to return near target in 2027 and 2028, the ECB may be cautious about tightening policy too aggressively.

The survey also points to weaker growth. Forecasters now expect the eurozone economy to grow by only 1.0% in 2026, down from the previous estimate of 1.2%. Growth is then expected to improve slightly to 1.3% in both 2027 and 2028. The downward revision reflects the negative impact of higher energy prices and geopolitical uncertainty.

For households, the report means prices may remain painful this year, especially for energy, transport, and basic goods. But the projected decline in inflation over the next two years suggests that the pressure could gradually ease if energy markets stabilize.

For businesses, especially in energy-intensive sectors, the coming months may remain difficult. Higher input costs, weaker demand, and uncertainty over interest rates could delay investment and reduce profit margins. However, a return toward 2% inflation would help restore planning confidence over the medium term.

The ECB will now have to decide whether this year’s inflation jump requires a stronger policy response or whether it should treat the rise as a temporary shock. That decision will depend on whether energy-driven inflation begins to affect wages, services prices, and consumer expectations.

In the end, the survey sends a mixed but important message: inflation is rising faster than expected in 2026, but forecasters still believe it can return close to the ECB’s target by 2027 and 2028. Europe may face a difficult year of higher prices, but the longer-term outlook remains more stable than the current numbers suggest.