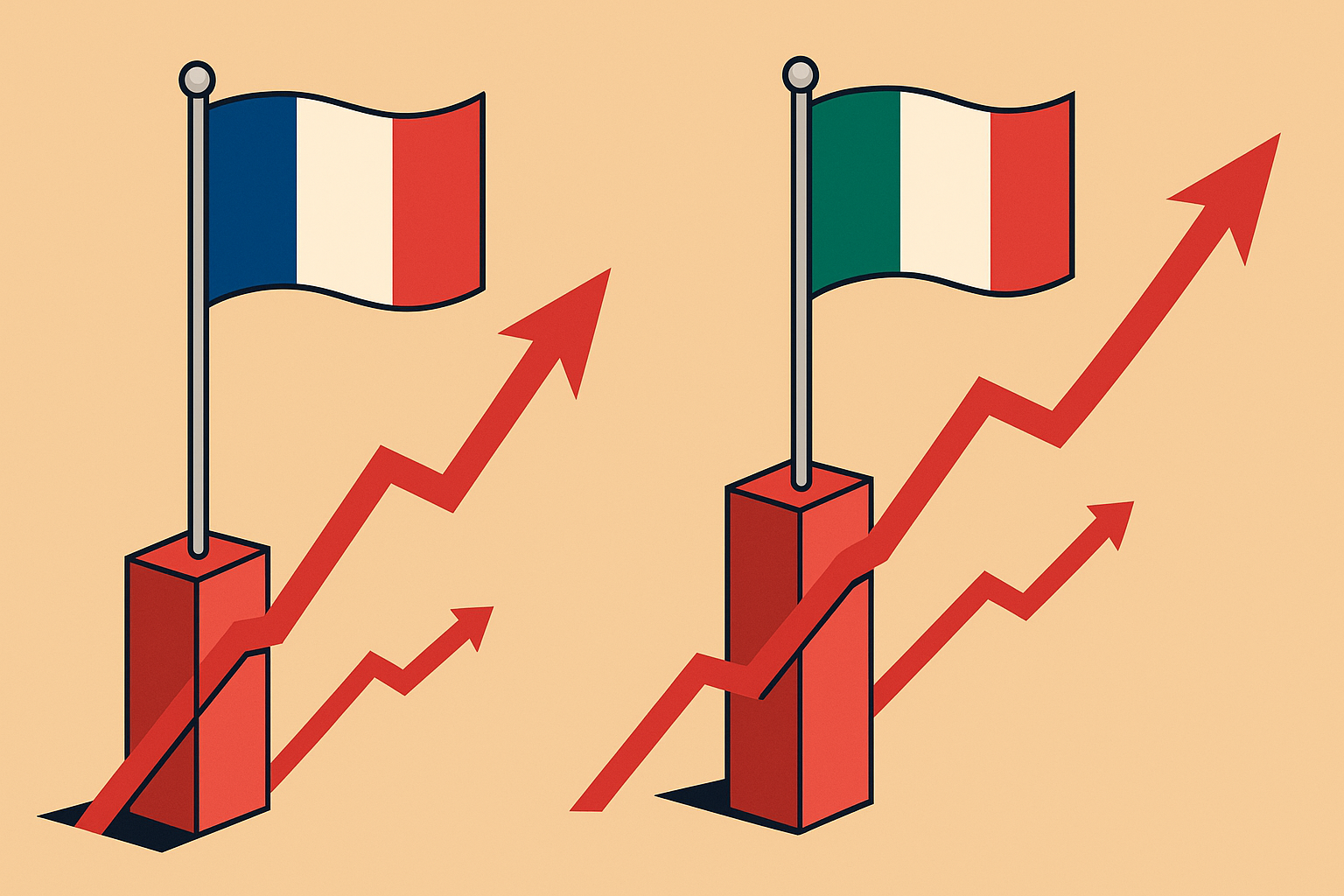

France’s long-term borrowing costs are approaching those of Italy for the first time since the global financial crisis, reflecting growing investor concerns over the eurozone’s second-largest economy.

Yields on 10-year French government bonds have risen above 3% over the past year, narrowing the gap with Italy’s equivalent bonds to just 0.14 percentage points. The shift comes as months of political instability and rising public debt weigh on France’s economic credibility.

This convergence challenges the long-standing perception of France as one of the eurozone’s safest borrowers and Italy as a higher-risk market. During the eurozone debt crisis of the 2010s, Italy’s yield spread over France exceeded four percentage points.

Analysts point to diverging fiscal trajectories. France continues to run large budget deficits, with a debt-to-GDP ratio of 113% in 2024, expected to rise to 118% by 2026. The country’s budget deficit reached 5.8% of GDP last year, far above the EU’s 3% limit, prompting credit rating downgrades and negative outlooks from major agencies.

Prime Minister François Bayrou has announced a €44 billion fiscal package of tax rises and spending cuts for 2026, describing it as a “moment of truth” to avoid a Greek-style debt crisis. However, with no parliamentary majority, the government faces significant challenges in securing approval. France recently endured a month without an approved budget after Bayrou’s predecessor, Michel Barnier, was ousted over his fiscal plans.

In contrast, Italy has benefited from relative political stability under Prime Minister Giorgia Meloni’s coalition. Fiscal restraint, including phasing out a costly “superbonus” home renovation scheme, has improved market sentiment. The budget deficit fell to 4.3% of GDP in 2024 and is projected to decline to 2.8% in 2025, meeting EU deficit rules and allowing Italy to exit excessive deficit procedures.

The spread between Italian and German benchmark bonds has narrowed to 0.8 percentage points, its lowest level since before the eurozone crisis, down from 2.5 percentage points at the time of Meloni’s 2022 election victory.

Market analysts note a shift in investor perception: formerly “peripheral” countries such as Italy and Greece now enjoy relative political calm, while political uncertainty and fiscal concerns have moved to the eurozone’s core, including France.